categories

All Categories

- Bitcoin

- Centralised Exchanges

- Crypto

- Crypto Asset Volatility

- Crypto Correlations

- Crypto Governance

- Crypto in the Portfolio

- Crypto Valuations

- DeFi

- ESG

- Ethereum

- Investment Highlight

- Regulation

- Security and Privacy

- Social Media Influence

- Stable Coins

- Traditional Finance and Crypto

- Uncategorized

- UNSDG

- Web 3.0

Authors

All Authors

Machines That Pay

by Quinn Papworth

For years, a small camp of crypto natives have argued that artificial intelligence and blockchains are natural partners. The thesis sounded esoteric when chatbots could only summarise emails. It sounds rather different now that software agents are beginning to act on their own.

This piece covers:

- Why agentic AI is structurally different from the chatbot era, and why it needs payment rails of its own

- Where the legacy banking system fails as infrastructure for autonomous software

- How the x402 standard is attempting to graft a payment layer onto HTTP — and the gap between its narrative and its actual usage

- The risks: prompt injection, malicious model routers, and the unresolved question of who is liable when an agent misbehaves

From advisor to actor

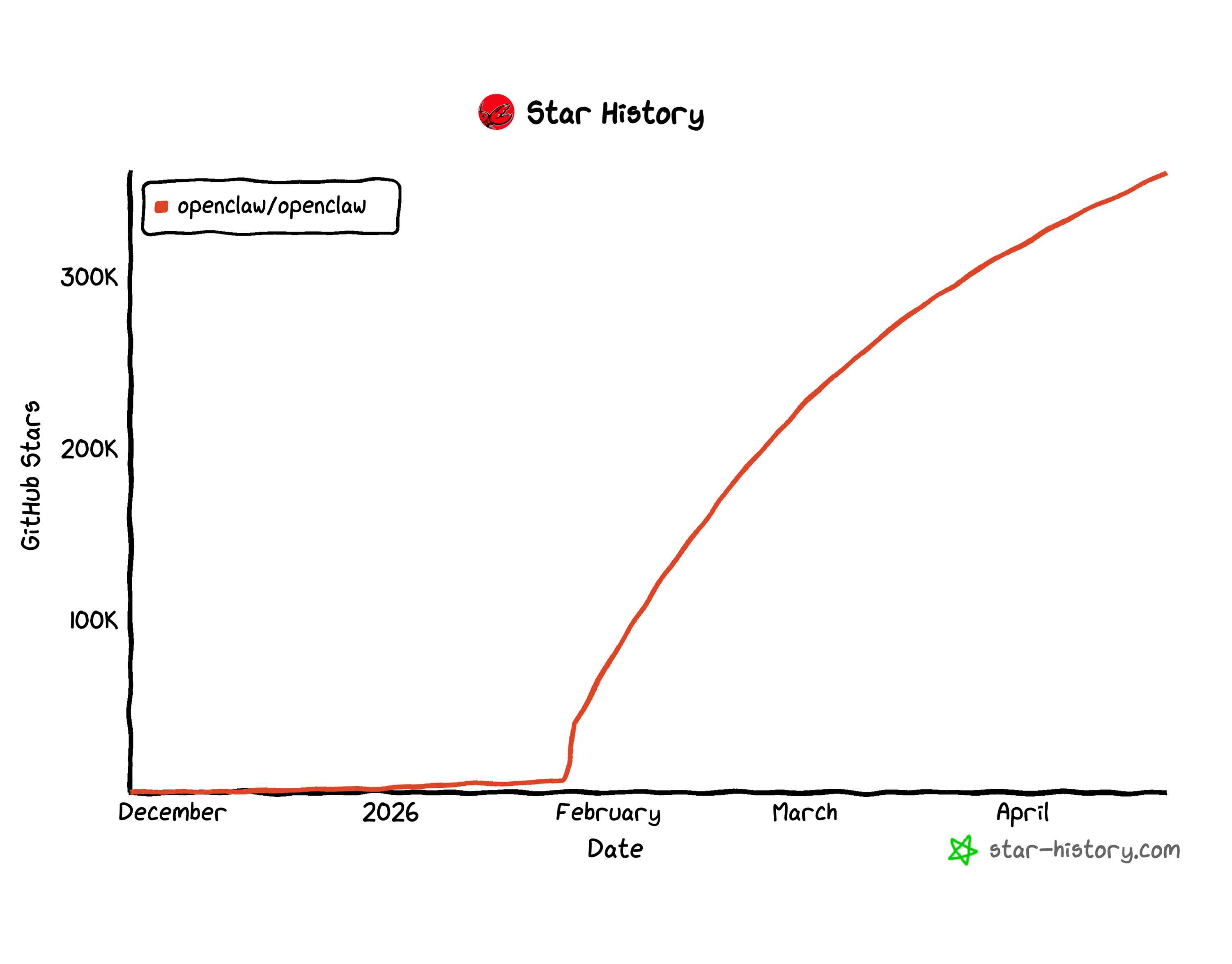

The release of OpenClaw, an open-source agentic framework that surpassed 250,000 GitHub stars within four months of its January launch, has done more to popularise the category than any white paper. Nvidia’s chief executive Jensen Huang told the company’s GTC conference in March that OpenClaw had “sparked the agent inflection point, extending AI beyond generation and reasoning into action,” and that every company would soon need an OpenClaw strategy. In China, queues formed outside Tencent’s Shenzhen headquarters as engineers helped install the software on the laptops of students, retirees and office workers.

The shift the software embodies is worth pausing on. A traditional chatbot, asked to tidy a chaotic email inbox, will produce advice: rules to set, folders to create, senders to mute. An agent, given the same instruction, opens the inbox, sorts the messages, archives the junk and reports back. The change is not in eloquence but in agency. Agents perceive an environment, decide on a course of action and execute it through whatever tools they have been granted, returning to their human principal only when blocked.

Agency, however, requires infrastructure. An agent that can read calendars but cannot pay for a calendar API, or that can research a flight but cannot book it, is a half-built thing. The question is which payment rails such systems will ride on. Here the existing financial system runs into trouble that is not a matter of polish but of design.

Why the bank rails do not fit

The mismatch begins with identity. To open a bank account, a customer must present a passport, a tax number and a face — credentials that an autonomous piece of software, by definition, does not possess. Workarounds exist: agents can be given access to a human-owned account. But that turns every agent into a delegated user of someone else’s identity, with all the legal and operational ambiguity that implies.

Settlement is the second problem. Card networks and bank transfers operate on human time — batched, business-hours, often delayed by days for cross-border flows. An agent that calls a thousand APIs an hour cannot wait for Tuesday to clear Monday’s bills. A third issue is programmability. Bank rails offer almost no native support for conditional payments, escrow, or logic-bound transfers. Whatever automation exists sits in the middleware layer, not the money itself.

Public blockchains invert each of these constraints. A wallet can be generated permissionlessly in milliseconds. Stablecoin transfers settle in seconds, around the clock, on chains designed for the purpose. Smart contracts allow payments to carry conditions: pay only on delivery, refund automatically on failure, release funds in tranches. None of this is exotic to anyone who has touched DeFi; what is new is that the user need not be a person.

x402: the payment layer the web forgot

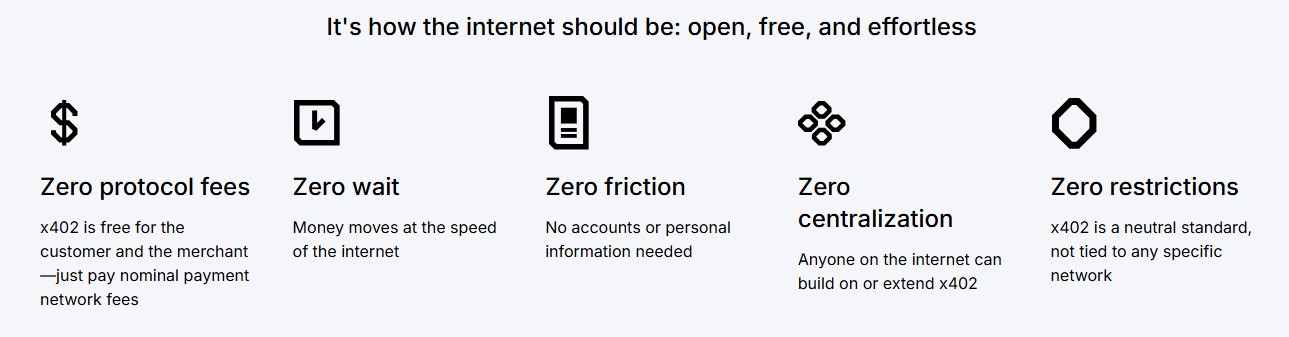

The most concrete attempt to wire all this together is x402, a protocol developed by Coinbase that revives an obscure piece of internet plumbing. The HTTP standard has long included status code 402, “Payment Required,” but it was never given a meaning. x402 supplies one.

The mechanics are straightforward. An agent makes an ordinary HTTP request — for a piece of data, a model inference, a premium API call, whatever. If the resource is not free, the server replies not with an error but with a 402 response containing a machine readable instruction: pay this many cents in USDC, on this chain, to this address. The agent settles the payment onchain, resends the request with proof, and receives the resource. The whole exchange completes in roughly two seconds. The protocol charges no fees of its own and supports any chain.

Adoption has, on the surface, been rapid. By March 2026, x402 had processed more than 119 million transactions on Base and 35 million on Solana, with an annualised volume of around $600 million across the ecosystem. The x402 Foundation, launched with twenty-two founding members including Visa and Google, has formalised the standard, and integrations now reach into Cloudflare, Stripe and AWS.

Beneath the headline figures, however, the picture is more sober. Onchain analysts at Artemis estimate that the protocol processes only around $28,000 in genuine daily volume, with much of the rest attributable to wash trades and infrastructure testing. Agentic AI payments currently account for roughly 0.0001% of total stablecoin volume, which itself reached $33 trillion in 2025. The plumbing is in place; the commerce is not yet flowing through it. Whether that gap closes is the question on which the entire thesis rests.

The risks that arrive with the rails

The same properties that make crypto rails useful for agents — permissionless accounts, instant settlement, irreversible transactions — make them dangerous when something goes wrong. The relevant attack surfaces are now well documented.

The first is prompt injection. Because large language models cannot reliably distinguish instructions from data, an attacker who can place text in front of an agent can often hijack it. A malicious instruction hidden in a webpage, a calendar invite or an email attachment can persuade an agent to transfer funds, leak credentials or alter its own future behaviour. Memory poisoning is a particularly insidious variant, in which the malicious instruction is implanted in an agent’s persistent storage and recalled in sessions days or weeks later.

The second is the supply chain around the model itself. A University of California study published in April 2026 tested 428 third-party LLM API routers and found that nine were actively injecting malicious code, seventeen were exfiltrating cloud credentials, and at least one had drained ether from a researcher’s wallet. Two routers used adaptive evasion, waiting fifty calls before activating to defeat behavioural monitoring. Hardware wallets and multi-signature schemes offer no protection against a compromised piece of middleware sitting between an agent and its model.

The third is governance. The x402 standard handles the question of how a payment is made, but not the question of whether it should be authorised. Galaxy Research projects business-to-consumer agentic commerce will reach between $3 trillion and $5 trillion by 2030, a scale at which the absence of robust spending policies, cryptographic identity and audit trails becomes a systemic concern rather than an academic one.

The legal questions are equally unresolved. When an autonomous agent executes a fraudulent payment, who is liable — the user who deployed it, the developer who wrote it, the model provider whose weights generated the decision, or the protocol that settled the transaction? No jurisdiction has answered this clearly, and the architecture of public blockchains, in which transactions cannot be reversed, makes the answer urgent.

The road ahead

The strongest version of the thesis is now demonstrably correct: agentic software does need payment rails of its own, and the rails it needs look much more like a blockchain than a bank. The weaker version — that this transition is already underway at a meaningful scale — is harder to defend. Most of the volume is still synthetic, most of the integrations are still experimental, and most of the security work has yet to be done.

What can be said with some confidence is that the direction of travel is set. Stablecoin volumes are now measured in tens of trillions of dollars a year. The world’s largest cloud providers, payment networks and AI laboratories have all aligned around a common standard for machine-to-machine settlement. The infrastructure is being built ahead of the demand, in the expectation that the demand will follow. That is usually how plumbing gets laid.

For investors, the practical question is not whether to believe the agentic-payments narrative but how to size positions against a thesis that is structurally sound but commercially early. The protocols, settlement layers and stablecoin issuers that benefit from machine-driven volume will, if the thesis plays out, potentially capture a meaningful share of a very large pie.

Quinn Papworth

Quinn holds a Bachelor of Business from RMIT, majoring in Finance & Blockchain Enabled Business and has 4 years experience actively investing in crypto markets. Quinn is an analyst at Apollo Crypto and is deeply passionate about producing accessible crypto research content to help educate and onboard users.