categories

All Categories

- Bitcoin

- Centralised Exchanges

- Crypto

- Crypto Asset Volatility

- Crypto Correlations

- Crypto Governance

- Crypto in the Portfolio

- Crypto Valuations

- DeFi

- ESG

- Ethereum

- Investment Highlight

- Regulation

- Security and Privacy

- Social Media Influence

- Stable Coins

- Traditional Finance and Crypto

- Uncategorized

- UNSDG

- Web 3.0

Authors

All Authors

Tokenisation – The $33bn Question

by Quinn Papworth

Real-world asset tokenisation is no longer a thesis; it is infrastructure. The interesting questions have shifted from demand to depth.

- Tokenised real-world assets ex-stablecoins have reached $33.7bn, more than fifteen-fold growth since the start of 2024

- BlackRock’s BUIDL alone holds ~$2.85bn, with JPMorgan, Fidelity and Franklin Templeton now shipping competing products

- America’s SEC is poised to permit third-party-issued tokenised stocks to trade on DeFi venues — a “Copernican” shift from the previous era

- The binding constraints are now liquidity fragmentation and secondary-market depth, not demand

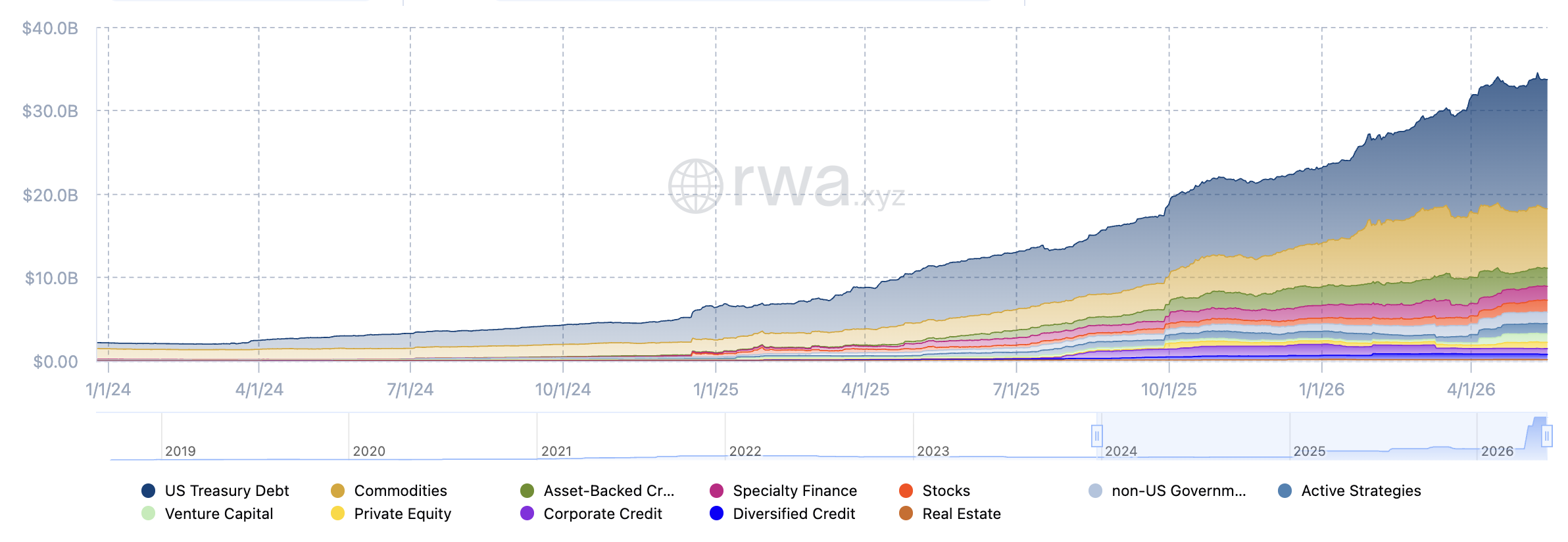

For a decade, “putting assets on the blockchain” was a phrase that inspired conference panels and little else. The pilots came and went; the demos were earnest; the volumes were rounding errors. That era is over. According to RWA.xyz, the distributed value of tokenised real-world assets — excluding stablecoins, which are a category unto themselves — stood at roughly $33.7bn in mid-May 2026, up from around $2bn at the start of 2024. The market has, at last, grown teeth.

It has also grown a familiar set of names. BlackRock’s BUIDL fund, launched in March 2024 with Securitize, now holds close to $2.85bn in tokenised Treasury bills and repos, lives across nine blockchains, and in February began trading on Uniswap — the first time the world’s largest asset manager has used a decentralised exchange as distribution infrastructure for one of its own funds. On May 8th the firm filed paperwork with America’s Securities and Exchange Commission for two further blockchain-native Treasury vehicles. JPMorgan launched MONY, its own tokenised money-market fund, on Ethereum in December with a $100m seed. Fidelity’s FDIT crossed $250m the same week. Franklin Templeton and Ondo have been in the market longer; Apollo Global, Citadel and a clutch of European banks are also involved.

Why now

The proximate cause of the surge is unglamorous: regulatory clarity. America’s GENIUS Act, which formalises a federal framework for payment tokens and stablecoins, removed the most acute legal ambiguity hanging over the category; the broader CLARITY Act hopes to do similar work for digital-asset market structure. Federal banking regulators issued guidance earlier this year confirming that a tokenised security carrying the same legal rights as its conventional counterpart will be treated the same way. That sounds banal. It is not. For a treasurer at a large bank, the calculus was never whether onchain settlement was technically superior — it plainly is — but whether her compliance department could sign off. Now it can.

The deeper drivers are structural, and they reward sitting with for a moment.

The first is operational arbitrage. Smart contracts collapse the post-trade infrastructure that consumes a significant share of asset-servicing budgets at incumbent custodians. Settlement moves from T+2 to near-instant. Coupon and dividend distribution becomes a function call rather than a reconciliation exercise. BUIDL distributes dividends daily, in token form, directly to holders’ wallets — a feat traditional money-market funds cannot match without a costly intermediary layer. For the issuer, the savings are real; for the holder, the yield arrives without friction.

The second is collateral mobility. Tokenised Treasuries are now accepted as margin on exchanges such as Deribit, as backing for many stablecoins, and increasingly as collateral inside DeFi lending markets. This matters because it solves an old problem: a Treasury bill earning 4.5% in a traditional brokerage account is dead capital for anyone who also wants leverage on a crypto position. Onchain, the same bill can now earn its coupon and post as margin simultaneously. That is not a marginal improvement. It is a different product.

The third is distribution. A token issued on Ethereum is, in principle, available to any wallet on Earth. Permissioning layers — whitelists, KYC gates, jurisdictional locks — can be added back, and for regulated products they invariably are. But the default geometry is global, not domestic, and that inverts the economics of fund distribution. Where the marginal cost of onboarding a new investor in a traditional fund is significant, on a public chain it approaches zero.

What is actually onchain

The composition of the market has matured beyond the early monoculture of Treasuries — though Treasuries still dominate. Of the $33.7bn in distributed value tracked by RWA.xyz in mid-May, US Treasury debt accounts for $15.5bn, or roughly 46% of the total. Commodities, dominated by Paxos Gold and Tether Gold, form the second pillar at $7.1bn, a category that has quietly grown into a structural hedge inside onchain portfolios rather than the curiosity it was a year ago.

Beyond those two giants, the market thins quickly. Tokenised credit splits across two buckets on RWA.xyz’s taxonomy — asset-backed credit at $2.2bn and specialty finance at $1.7bn — together forming a roughly $3.9bn onchain private-credit complex.

Five further categories have crossed the $1bn line in distributed value: tokenised stocks ($1.4bn), non-US sovereign debt ($1.4bn), active strategies ($1.2bn) and, newest to the list, venture capital ($1.0bn). Below that, private equity ($757m), corporate credit ($678m) and diversified credit ($626m) trail. The most striking laggard is real estate, at just $163m — perennially the category prophesied to lead tokenisation, perennially the one that does not. Property’s legal, custodial and valuation frictions have proved stubbornly resistant to a blockchain solution.

Ethereum remains the dominant settlement layer, hosting roughly 55–65% of tokenised value depending on the measure. BlackRock’s Larry Fink, in the firm’s 2026 thematic outlook, was unusually pointed about this: Ethereum, he wrote, commands the lion’s share of tokenisation infrastructure and is therefore the network of choice. Solana, Avalanche, Polygon and a handful of permissioned chains take the rest.

The equities revolution, with caveats

Tokenised equities are the most consequential new entrant, and they are about to become more interesting still. Ondo’s Global Markets platform launched in early 2026 with more than 100 tokenised US stocks and ETFs, including Apple, Nvidia, Tesla and broad-market index trackers. By mid-May, RWA.xyz tracked more than 2,200 distinct tokenised stocks across the various platforms. The total onchain value remains modest — comfortably over $1bn — but the trajectory matters more than the level. A retail investor in Jakarta or Lagos can now hold fractional Apple shares, settled onchain, without ever touching a US broker-dealer.

This week the SEC is expected to make that trajectory considerably steeper. According to a Bloomberg report on May 18th, the agency under Chair Paul Atkins is preparing to release an “innovation exemption” — a regulatory sandbox lasting 12 to 36 months — that would allow tokenised stocks to trade on DeFi platforms under lighter requirements, dispensing in some cases with full broker-dealer or exchange registration. The exemption follows approvals granted to Nasdaq’s tokenised securities framework in March and to NYSE’s equivalent in April, both of which kept tokenised trading within the existing market plumbing via the Depository Trust Company’s tokenisation pilot. The innovation exemption is the more radical sibling: it targets onchain trading outside that perimeter, on permissionless public blockchains and automated market-makers.

The detail that has caught Wall Street’s attention is the SEC’s apparent willingness to permit tokens that do not confer shareholder rights. Under the framework, third parties could issue tokens linked to public equities without authorisation from the underlying company, provided the tokens trade on platforms that meet KYC, anti-fraud and whitelist requirements. Platforms could lose their exemption if listed products fail to provide voting or dividend rights — but the structural concession has already been made: synthetic exposure to listed equities, issued by third parties, is now a legitimate onchain instrument.

For DeFi this is transformative. Tokenised stocks without issuer consent removes the single largest practical bottleneck in the category. One does not need to negotiate with Apple to list an AAPL-linked token; one needs only the underlying shares in custody, or a derivative structure that references them. The implication, if the rules land as drafted, is that the universe of trade-able onchain equities expands from a few hundred negotiated products to, in principle, the entire S&P 500 — and trades on a Uniswap-style automated market-maker rather than a regulated exchange.

It is also, however, a category invitation worth scrutinising. A tokenised equity that carries no voting rights and no dividend pass-through is not really an equity; it is a derivative dressed in equity clothing. The economic exposure tracks the underlying, but the legal architecture is closer to a contract for difference than to a share. That distinction has not mattered in normal markets. It will matter the first time a tokenised-equity issuer fails to honour redemption, or a smart-contract bug breaks the link between token and underlying, or a tokenised-stock platform faces a stress event with no recourse to the issuing company. The SEC’s stance acknowledges the trade-off explicitly — it is permitting “betting on the fortunes” of public companies, as Bloomberg’s wording put it, not granting onchain shareholding. Traders and protocols would do well to take the agency at its word.

The cracks

It would be too neat to end here. The market has scale; it does not yet have depth. A recent academic study of more than $25bn in tokenised RWAs found that secondary-market activity remains thin across most categories: onchain transfers tend to cluster around $10m, the signature of institutional allocation batching rather than continuous trading. Issuance, in short, has outpaced trading. Many tokenised assets behave less like liquid securities and more like digitised certificates that occasionally change hands.

Fragmentation is the second cost of growth. With identical assets now issued across nine or more chains, prices for the same instrument can diverge by 1–3%, and moving capital between networks introduces further friction. This is the unglamorous tax of a multi-chain world, and no party — issuer, exchange, bridge operator — has yet solved it convincingly. Wormhole and similar interoperability layers help; they do not eliminate the problem.

Other constraints are familiar from the wider crypto literature. Oracle reliability remains a single point of failure for any token whose value depends on off-chain pricing — a concern that intensifies as synthetic-exposure tokens proliferate. Regulatory treatment varies sharply between jurisdictions: an instrument that is plainly a security in America may be a payment token in Singapore and a regulatory void elsewhere. Custody arrangements for institutional holders — Anchorage, BitGo, Fireblocks, BNY Mellon for BUIDL’s cash leg — are workable, but the legal status of tokens in bankruptcy remains under-tested.

Looking Forward

Tokenisation has crossed the threshold that matters: it is now boring. Boring is the highest compliment one can pay a piece of financial plumbing. When BlackRock files routine SEC paperwork for two more onchain Treasury funds, when JPMorgan seeds its own with a hundred million dollars, when federal banking regulators issue guidance treating tokens as their conventional analogues, the story has shifted from disruption to integration. The $33.7bn figure is a fraction of the $100trn-plus addressable pool, and most credible projections to 2030 — Grayscale, BCG, McKinsey — land in the low-trillions range.

Quinn Papworth

Quinn holds a Bachelor of Business from RMIT, majoring in Finance & Blockchain Enabled Business and has 4 years experience actively investing in crypto markets. Quinn is an analyst at Apollo Crypto and is deeply passionate about producing accessible crypto research content to help educate and onboard users.